Currencies are the heart of forex trading. While on most days, currencies tend to fluctuate, large movements such as those seen in the equity markets are a rare occurrence.

Yet, there are moments, when currencies react to major shocks in the financial markets. It may be a deliberate shock, in an effort to achieve a goal. In most cases, currency crises are a result of government mismanagement as well as speculation.

Times such as these can put a forex trader on the edge. They are indeed Black swan events. At times one can perhaps foresee what is to come, but in some cases, currency crises can catch many off guards.

In this article, we aim to explain some of the biggest currency collapses in recent memory. While it serves the purpose of making for an entertaining read, traders also have lessons to learn. The most obvious comes from risk management.

Yet, there are cases where even the astute trader would have had a sleepless night. No amount of risk management or currency hedging would prepare one to come out unscathed. Currency crises often happen in tandem with other impacts.

Therefore, a currency crisis doesn’t just happen in isolation. Many times there are well-grounded reasons for a currency to behave the way it does. During some of the major financial crises in the past, it isn’t just the equity markets, but even forex markets that feel the impact.

The three currency crises that we present in this article, in most cases are the main driver. Meaning that it was the currency market crisis that led to a wider impact on the financial markets.

Hence, these case studies stress on the importance of keeping an ear to the ground when it comes to forex.

What causes a currency crisis?

Before diving into the three currency crises, we should first understand what qualifies as one.

A currency crisis is defined as a sudden and in most cases, the unexpected change in the value of a currency.

Many tend to use the word "rapid decrease" even though a rapid appreciation of the exchange rate can trigger a crisis. This is because of the status of an economy. For an import-oriented economy, a stronger currency makes importing goods cheaper.

For such economies, a rapid depreciation in the exchange rate makes the cost of imports more expensive. It affects factors such as the balance of payments and inflation among other things.

On the opposite end, an export-oriented economy prefers a weaker exchange rate so as to make its goods more competitive in the global markets. For such economies, a rapid appreciation in exchange rates can make their exports less enticing.

The keyword is the speed at which the currency rises or falls. When there is a disconnect between economic growth and the exchange rates, it leads to a massive fallout.

In some cases, a currency crisis is caused deliberately. This is when central banks intervene. There are many examples of central banks intervening in the currency markets.

In many cases, policymakers make statements to the media. This is often the simplest and doesn’t require and special monetary policy tools. It works time and again, but the context is very important.

For example, RBNZ President Graeme Wheeler said in August 2017 that a “weaker New Zealand dollar was needed to help bolster its export sector.”

As evident from the NZDUSD price chart above, the Kiwi fell almost 6% in the months following his comments. Such types of verbal interventions typically do the trick, but in some cases, more is required.

The Russian rouble crisis of 1998

The 1998 Russian currency crisis is the most notable in recent times. It follows the aftermath of the fall of the Soviet Union in 1991. One of the key aspects of this crisis was the peg to the US dollar.

Also known as a pegged currency, this is when a currency has a fixed exchange rate for another currency. Whenever the currency moves outside of the range, central bank, such as the Russian central bank would intervene

After Russia opened up to the world, it saw foreign investment pouring into the country. But the Asian financial crisis saw investors take a more prudent approach. Inevitably, as a consequence of the Asian financial crisis, the Russian rouble took a hit.

To encourage investors to hold on to the rouble-denominated assets, the central bank hiked interest rates to 150%. On the flipside, this also raised Russia's debt which eventually grew higher than its tax receipts.

The interest rate move had a negative effect spooking investors even more and enticing them to sell the rouble. By 1998, the chickens came home to roost, in a perfect culmination of fears of a default and talks of possible currency devaluation.

Since the RUB was still pegged to the USD, the central bank continued to intervene, but it eventually gave up defending the peg in September 1998. This led to the rouble becoming a freely floating exchange rate for the dollar. In about three weeks, the currency lost two-thirds of its value.

Although this caused a lot of pain in the years ahead, the free-floating rate meant that it reflected the true market value of the currency.

To learn more about the Russian currency crisis and the default of 1998, this case study from the St. Louis Fed makes for an interesting read.

The Swiss franc de-peg to the euro

In 2015, on a fine Thursday morning in January, the Swiss Central Bank truly jolted the markets. It announced that it officially abandoned the peg to the euro, sending the CHF to pop. The peg was set at 1.20 CHF

This comes just after four years when in September 2011, the central bank announced that it was pegging the CHF to the euro. The decision was made in an effort to make Switzerland's exports more competitive. The country was expensive, to begin with, and the stronger CHF made exports even more difficult. Furthermore, the euro was reeling under the crisis and the single currency weakened quite a bit.

The Swiss de peg to the euro came truly as a surprise to everyone. It was just days before that one of the central bank officials reiterated the SNB's commitment to the peg.

The EURCHF exchange rate plummeted, as the CHF surged, falling over 20% and falling to parity before recovering in the days later. The chart below shows the EURCHF movement on January 2015. The decision impacted not just the EURCHF, but it strengthened the Swiss franc on the whole.

This meant that similar moves were seen across USDCHF and other CHF currency pairs as well. The impact was much closer home as it immediately bankrupted many brokers, especially those who were operating under a variable or a floating spread model.

Consequently, CHF became expensive overnight. The decision is well covered across various media outlets. But this comment from Thomas Jordan, the SNB chief at the time stood out “If you decide to exit such a policy, you have to take the markets by surprise…”

The move came just under a month after the Swiss national bank introduced negative interest rates for the first time.

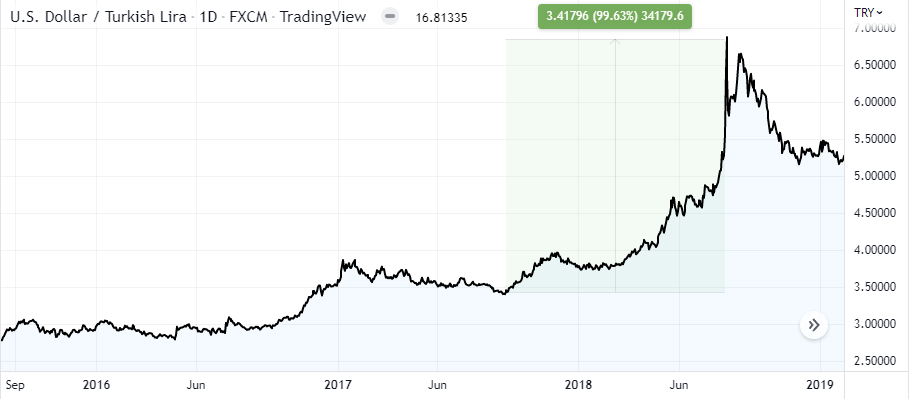

2018 Turkey currency crisis

In recent years, we have heard a lot about the Turkish lira. However, Turkey is not new to a currency crisis. One of the most recent crises was the currency and debt crisis in 2018.

The lira hit record lows as it pushed up prices of goods and services in the country. While it was a boon for tourists, it wasn't enough to help offset the negative effects of a weaker currency.

The Turkish currency crisis is not that happened overnight but has been a crisis in the making for a while. The lira depreciated steadily against the USD since January of 2018, eventually plummeting to 6.8 to the dollar.

The impact was seen elsewhere as well, with the Turkish equity market falling 17% and also pushing sovereign borrowing costs higher. Leading to this bust was the heavy borrowing in the country. Boosted by a boom in the construction sector, Turkish companies began to borrow heavily, issuing bonds in EUR and USD denominations.

Around the time, the worsening relations between then US President Donald Trump and President Erdogan also made things difficult.

President Trump had made a tweet about approving a doubling of tariffs on Turkish steel and aluminium imports. Alongside the geopolitical tensions, the economic policy of Turkey also came under harsh criticism.

For one, investors believed that the nation's monetary policy was heavily influenced by the President. Many central banks around the world enjoy a certain level of independence. This was clearly lacking when it came to Turkey.

The currency depreciated almost 100% in a mere twelve months, from September 2017 onward.

The USDTRY exchange rate is now more than double the exchange rate in 2018, at 16.81. However, it was the somewhat rapid movement in the exchange rate that made everyone take notice.

Currency crisis – Fixed rates, a common theme

Besides the above three examples, there are many other instances. For example, the euro plunged during the peak of the Greece sovereign debt crisis. The British pound fell sharply after Brexit and there are many such examples around the globe.

There can be many reasons behind the currency crisis, which as we covered and showed in the examples can sometimes be deliberate, and at times completely unexpected. In cases such as Brexit, the drop in the British pound was the result of a conscious decision to leave the EU.

However, one common theme of the crisis is the fixed exchange rate. A fixed exchange rate doesn’t mean a hard peg, but rather has a little bit of room for the currency to deviate from the peg.

Over the years, many countries learned the hard way of adopting a free-floating exchange rate. Even to this day, there are many currencies that follow a fixed exchange rate policy.

Many currencies, especially those in the Middle East have a fixed currency rate against the US dollar. When it comes to the euro, the Danish krone is pegged at 7.46, while a big name from Asia is the HKD, which is pegged to the USD at 7.80.

The Chinese yuan follows a somewhat similar model, with the additional comfort of being allowed to move 2% from the peg to the US dollar. It also has additional controls in place such as capital controls to help during times of crisis.

During normal times, the fixed exchange rate works well, providing stability. However, it is during times of crisis that the fixed exchange rate can be tested. It can get even more difficult as speculators often jump in, worsening conditions for the currency that is following a fixed rate.

Lessons that traders can learn from a currency crisis

As retail forex traders, a currency crisis can either make or break you, depending on which side of the market you are on. But having said that, such a crisis can also offer a great potential to make a windfall if you get it right.

The Swiss franc shock for example led to many traders owing money to their brokers. On the other hand, those who were long on the CHF made huge profits partly because of no stops being triggered due to lack of liquidity in the market.

Risk management is of course essential when trading in such market conditions. However, it is not as simple as just going long or short depending on which way the wind blows. A trader needs to have a good understanding of what is going on in the markets, should they wish to take advantage of such large movements in the currency markets.

Additional factors such as leverage and positions play an important role, in keeping the balance between a margin call or being deep in the profits. While currency crises are not that common, when they do happen, it can create some unique trading opportunities.